Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

not featured

2024-10-31

Credit

published

How Cash-Out Refinances Can Help Homeowners with Debt Relief

-

-

High-interest debt can feel like wearing a backpack filled with bricks while trying to run a marathon. With today’s rising living costs and ongoing economic uncertainty, many people are struggling to keep up with their financial responsibilities. Credit card debt, in particular, is a common issue that can quickly spiral out of control if not handled early on. But how do you reduce credit card debt? Keep reading while we explore how cash-out refinances can offer a lifeline to homeowners with debt.

Credit Card Use in the United States

It's no secret that in America, credit cards are as common as coffee on a Monday morning. In fact, according to the Federal Reserve, 82% of Americans held at least one credit card in 2023, with the average person juggling about 3.9 cards.1,2

Adults often rely on credit cards for everyday expenses, emergencies, and larger purchases. Unfortunately, many cardholders are also in debt, often without a plan to pay it off.

.png)

Credit Card Debt Statistics

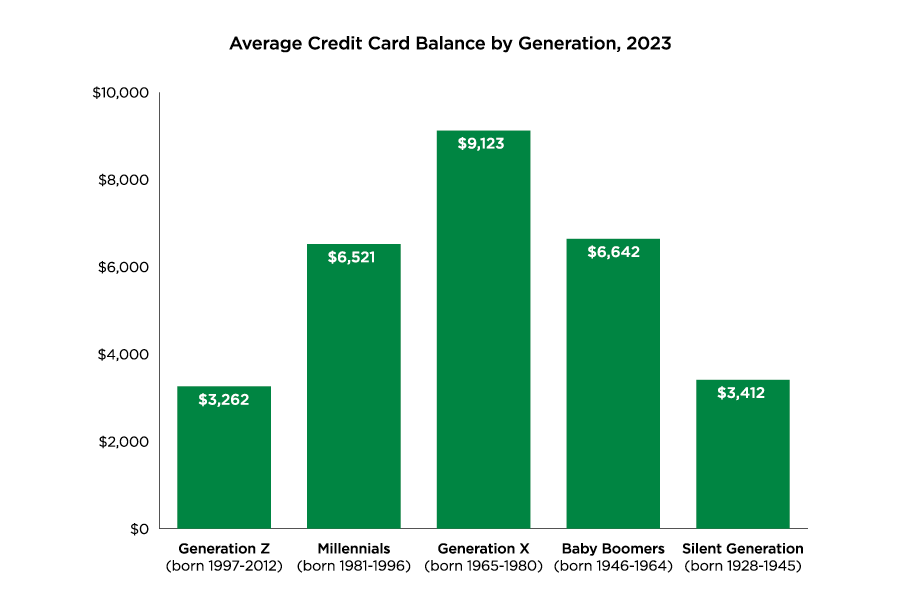

By Q2 2024, credit card debt in the U.S. hit over $1.14 trillion, with the average cardholder owing around $6,501.3,4 Interestingly, Generation X has consistently carried the most credit card debt over recent years.

Here’s a quick look at the average credit card balances by generation in 2023:

.png)

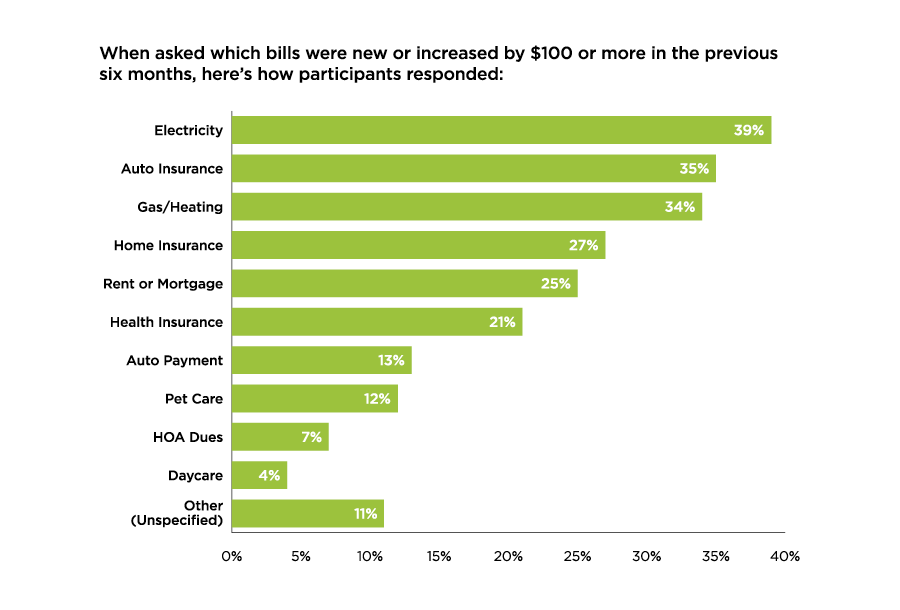

What Factors Contribute to Credit Card Balances?

In a recent Experian survey, 58% of respondents noticed a significant jump in their monthly expenses.4 Many cited that these rising costs are impacting their ability to pay down their credit card balances. Here’s a breakdown of the bills that saw the biggest increases:

Challenges in Paying Off Debt

As essential expenses rise, many people are relying more on credit cards. Even more concerning, most don’t believe they can pay off this debt within the year.5 Some of the major hurdles include:

- Rising Costs: 50%

- High Interest Rates: 43%

- Lack of Emergency Funds: 32%

- Large Necessary Expenses: 32%

- Inability to Cover Basic Necessities: 26%

- Job Instability: 21%

The Impact of High Interest Rates

High interest rates on credit cards make it even harder to pay off debt. This means even when you are making payments, a big chunk goes to interest rather than chipping away at the actual debt.

The mental aspect of living with debt also shouldn’t be ignored, especially because it takes a toll on your health. Individuals often face unwelcome side effects, including difficulty sleeping, higher anxiety levels, social isolation, and depression due to their debt.6

Cash-Out Refinancing: A Potential Debt Solution

For homeowners struggling with high-interest debt, cash-out refinancing can be a game-changer. This process involves refinancing your existing mortgage for more than you owe and taking the difference in cash. Then, this extra cash can be used to pay down high-interest credit card debt.

The benefit? Mortgage interest rates are typically much lower than credit card rates. For example, in July 2024, the average 30-year fixed mortgage rate was 6.73%, about 20% lower than the average credit card interest rate.7 This means you shouldn’t waste your time paying excessive interest on credit cards when you could get a cash-out refinance instead.

Plus, the most recent cuts in interest rates by the Federal Reserve could make this an even more appealing time to consider a cash-out refinance.8

Academy Bank’s Cash-Out Refinances for Debt Relief

If you are a homeowner feeling bogged down by credit card debt, a cash-out refinance might be your ticket to relief. By tapping into your home equity, you could access funds at a lower interest rate and lighten your debt load.

At Academy Bank, we understand the struggle of managing high-interest debt. If you are curious about cash-out refinancing* and how it can benefit you, our experienced lending team is ready to guide you toward a debt-free future. Let’s tackle this together!

1 Board of Governors of the Federal Reserve System, “Economic Week-Being of U.S. Households in 2023.” May 2024. https://www.federalreserve.gov/publications/files/2023-report-economic-well-being-us-households-202405.pdf

2 Horymski, Chris. “What Is the Average Number of Credit Cards?” Experian, April 24, 2024. https://www.experian.com/blogs/ask-experian/average-number-of-credit-cards-a-person-has/

3 Center for Microeconomic Data, “Quarterly Report on Household Debt and Credit.” Federal Reserve Bank of New York, August 2024. https://www.newyorkfed.org/microeconomics/hhdc.html

4 Horymski, Chris. “Average Credit Card Debt Increases 10% to $6,501 in 2023.” Experian, March 11, 2024. https://www.experian.com/blogs/ask-experian/state-of-credit-cards/

5 El Issa, Erin. “2023 American Household Credit Card Debt Study.” NerdWallet, January 8, 2024. https://www.nerdwallet.com/article/credit-cards/average-credit-card-debt-household

6 Horton, Cassidy. “The Silent Strain: How Debt Takes A Toll On Mental Health.” Forbes, September 25, 2024. https://www.forbes.com/advisor/banking/american-debt-and-the-mental-health-epidemic/

7 Karl, Sabrina. “Mortgage Rates Fall Back to 3-Month Low.” Investopia, July 18, 2024. https://www.investopedia.com/mortgage-rates-fall-back-to-3-month-low-july-18-2024-8679759

8 Neubauer, Kelsey. “How much will the Fed cut rates?” CNBC, September 17, 2024. https://www.cnbc.com/select/when-will-interest-rates-drop/

Member FDIC

* Subject to credit approval. The Cash-Out Refinance loan product has specific terms and conditions. Fees apply. Must own home 6 months or greater or if paying off existing first lien mortgage then lien being paid off must be seasoned at least 12 months.